Norway

Everyone wants to be like Norway - large sovereign wealth fund, and a high tax rate on natural resources. But no one wants to do the hard work (& time) required to get there.

Let's see what they have:

- State Owned Oil Company - Think Woodside, or BP, but government owned & operated. Equinor explores for oil, operates facilities, builds pipelines, and sells product for profit. Publicly listed, Norway owns 67%.

- Direct Equity - The government holds a separate vehicle, the State Direct Financial Interest (SDFI), which takes direct ownership in every licenced oil area. The government puts up cash equal to the private companies investing in oil production.

- Stability - the 78% petroleum tax has been in place since the 70s, and has not changed at all since then. Companies can model returns on a 30 year project with confidence.

The 78% tax rate does not exist in isolation. It's one part of a complete system. All of this together has created the ecosystem, incentive and cashflows to add to a sovereign wealth fund.

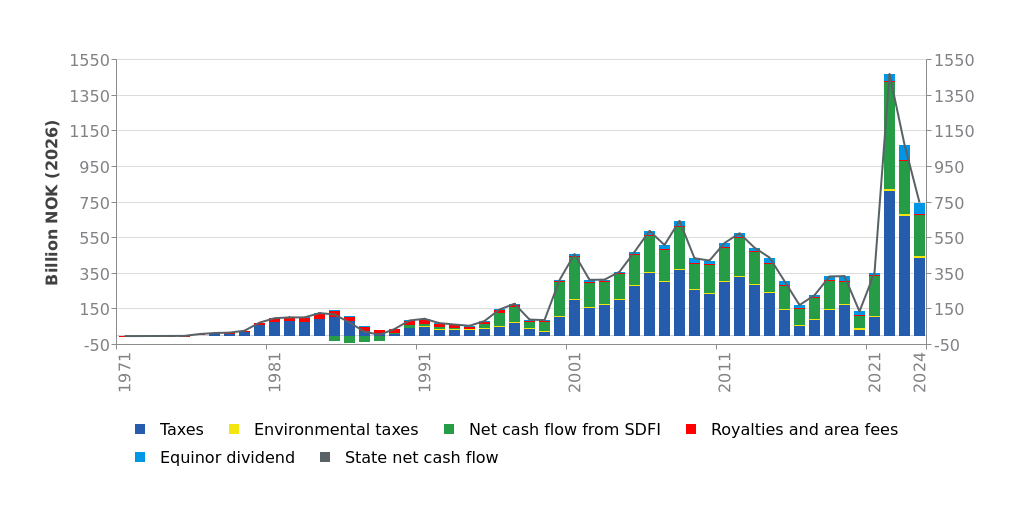

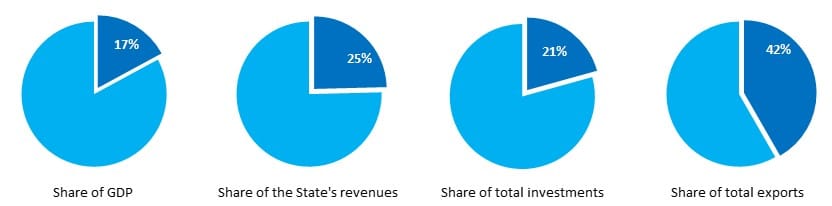

Norway keeps a detailed breakdown of all the revenue, jobs, GDP impact and related here, including this amazing chart. Revenue comes from multiple sources, and has swung widely over time.

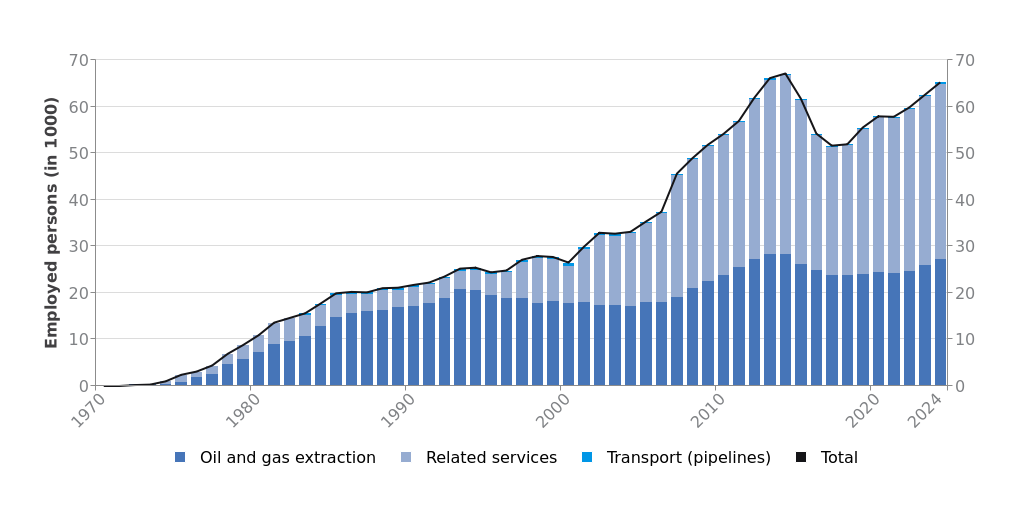

Direct Employment has been increasing over time and in 2025 now stands at 65,000 people. Indirect employment (retail, IT, employment agencies, machinery and equipment, hotels, restaurants, legal and accounting services) employs over 210,000 people (over 10% of all employment) and is a vital contributor to GDP.

History

Norway started offshore oil exploration in 1962, when Phillips Petroleum approached Norway to explore the North Sea, in return for exclusive rights. The government rejected their proposal outright.

In 1965, they started licencing exploration blocks, with standard terms (10% royalty, company tax only). All exploration and drilling was done by international oil companies.

Then came Ekofisk. After Philips Petroleum drilled 33 exploration wells and found nothing. They did one final drill and boom - one of the largest offshore wells ever discovered, estimated to hold 7 billion barrels of oil.

Norway realised they were sitting on a potential gold mine and took their shot. In 1972- the parliament setup a fully integrated system. Government owned oil company (Statoil), the ‘Ten Oil Commandments’ (a set of principles that included mandatory onshore processing and no flaring of gas’ and mandated 50% government equity involvement in all licences going forward. All with bipartisan agreement.

Note - They DID NOT apply these retrospectively, only to new licences.

Then in 1975, the 78% tax rate was applied, and government took control of the ‘norm pricing’ so companies could not game the system with offshore transfers and intra company pricing games. The oil companies complained at the time, but the government did not sway.

Then in 1990 they created their Sovereign Wealth Fund, however first capital transfer was only 1996. Then in 2001 the listed the Government Oil Company (Statoil, then Equinor) on the share market, keeping 67% ownership.

The UK

You can't find a better comparison to Norway then the UK. They literally share the same North Sea basin, split in half in 1965: everything to the east went to Norway, everything to the west to the UK. Both countries started oil production in the early 70s.

And, the UK copied Norway's approach, creating a government oil company, British National Oil Corporation (BNOC) in 1976, to develop and drill for oil.

Then came Thatcher. In 1982 BNOC was privatised (as Britoil), and by 1988 it was absorbed into BP. The Central Policy Review Staff with the U.K. cabinet office did not like the sale, and that oil assets "are almost certain to rise in price in the years ahead." LINK (Note the headline - "Did the U.K. Miss Out on £400 Billion Worth of Oil Revenue?") Thatcher did it anyway.

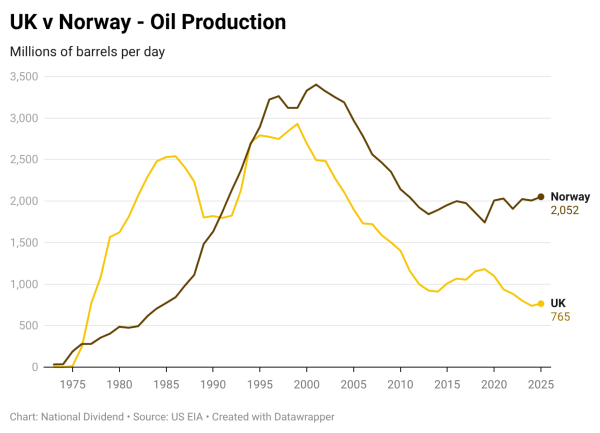

As you can see below, UK oil production peaked in 1999, plummeting down 69% to the low in 2014. Today it's even lower and still declining.

In 2014, the UK government was worried about the decline (revenue goes straight to government, no wealth fund there), commissioned Sir Ian Wood (the country's most senior oil industry figure) to review what had gone wrong. REPORT

Key Issues:

Lack of focus on Maximising Economic Recovery for the UK - "under the current approach, operators have pursued individual commercial objectives in insolation with limited shared commitment or obligation to maximise economic recovery across fields and regions within the UKCS (UK Continental Shelf)

Fiscal Policy - 'fiscal instability has been a significant factor in basin under-performance' - aka constantly changing laws & tax rates.

Government Stewardship - "The current model ('light touch')... will not be adequate to manage challenges the UKCS faces in the future'

Industry Stewardship - "the rapid fall in production efficiency is an indication of poor asset stewardship which the Regulator has not been able to adequately confront.."

Private companies, operating in their own self-interest, 'cream-skinned' the basin, took the easy cheap oil and left the rest. Infrastructure was built for their own use and not for the common good that the Norway system encourages.

Fiscal Policy - changing the tax rates. The UK had a 'Petroleum Revenue Tax' initially set at 45% in 1975. It was then moved to 60%, then 70%, then down to 50%. A Supplementary Charge was introduced, removed, then back at 10%, 20%, 32%, 20%, then 10%. PRT dropped to 0 in 2016. 2022 an Energy Profits Levy was introduced at 25%, then raised to 35%, then 38%.

15 changes in 50 years - and the current effective rate is 78% for Oil & Gas projects.

How do you plan for this? How do you make a multi-billion dollar investment when you have no idea what the tax rate will be 1y, 5y, 25 years away?

Norway has had the same top-level rate for oil & gas - 78%, since 1975 (as they cut company tax rate, they increased the levy so it remains the same).

What's worse is the future outlook.

From 2016 to 2025, Norway drilled 279 exploration wells and found 2.6 billion barrels of new resources. Britain drilled 79 wells and found 370 million.

In 2025 Norway spent 273 billion Norwegian crowns (US$28.8 billion), a record amount, in oil and gas activity and pipeline transportation, up by 8.7% compared to 2024. The UK spent £4.8 billion (US$6.3bn), a decrease from the £5.95 billion invested during 2024.

Summary

If you look beneath the hood, Norway has built a complete system to extract maximum value from their natural resources:

- Bipartisan political agreement. The Ten Oil Commandments were adopted unanimously. Parties agreed not to campaign on them. The framework has survived multiple governments for over fifty years.

- A government-owned oil company. Funded through eight years of losses before it turned its first profit. Statoil's staff were embedded with foreign operators, learning on the job, with a contractual right to take over operatorship after ten years. By 1987 it was running one of the largest offshore fields in the world.

- 50% government equity in all exploration areas. Equal ownership, equal risk of loss, and equal capital contributions.

- Shared infrastructure designed for national benefit. Norway organised the pipeline backbones, onshore processing plants, ocean platforms, and transport systems so that every new field could tie into existing facilities rather than building from scratch.

- Managed, gradual licensing. Still releasing new exploration areas today, always adjacent to existing infrastructure. "Hurry slowly." Norway drilled 49 exploration wells last year.

- A tax regime that is stable, transparent, and non-gameable. No changes to the rate, and the government sets the taxable price, not the companies.

Norway embraces the oil & gas industry, encourages development, spends money and as a result has reaped the rewards with employment, career development and the large sovereign wealth fund. Norway Government

Look to Australia today. People are calling for at 25% extra tax on our gas exports. Ignoring the legalities of the contracts already signed, let's look at this for a moment:

- Will this raise additional revenue? Yes.

- Will this be a bi-partisan agreement, that won't be changed in the future? No.

- Will it be part of a system wide government led development program to explore and fund new fossil fuel developments? No.

- Will the government fund shared infrastructure to benefit all participants? No.

If you want the maximum value captured by government for the citizens of this country, look to the complete, bi-partisan system Norway have kept in place for 50 years. The tax (which should be higher for all natural resources) is only one part of it.

*As an aside - look at that last point: shared infrastructure.

Queensland LNG has 3 monster export facilities, all with their own infrastructure. There are 3 huge gas pipelines from the fields, own plants, storage facilities, jetties and so on. The combined cost of these three facilities (Australia Pacific LNG, Queensland Curtis LNG, and Gladstone LNG) was approximately $70 billion.

A 2017 industry analysis estimated that roughly $10 billion could have been saved on that combined cost by using shared facilities. Bloomberg.

This is a fascinating story on its own and more will come, including how the QLD and AUS governments ignored any advice to force a domestic gas reservation amount.

A government investment vehicle (Norway SDFI Equivalent) could have bought 10% of each project at the time, taken the gas produced as domestic supply, and worked together to avoid the duplication and saved money for all parties.